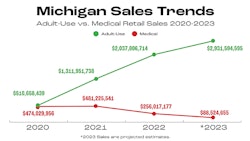

In the four years since its adult-use sales launched, Michigan has grown to become the second-largest cannabis market in the U.S., behind California. A highly competitive market with more than 2,100 active adult-use licenses, including 1,050 grower and 734 retailer licenses, it’s gained a reputation as a state that’s difficult to make money in. From June to October, another 72 grower licenses were issued, according to data from the state’s Cannabis Regulatory Agency. Yet, in 2023, Michigan’s adult-use market alone generated more than $250 million in sales each month since June 2023. With a population of 10 million, a summer tourist surge and friendlier business regulations than other legal states, the market has reached impressive maturity in its four years.

For consumers, it’s an oasis of variety at lower prices compared to other markets. When the price of a retail ounce of flower dropped to under $200 in late 2021, consumer purchasing on the legal recreational market skyrocketed, from 45% in Q3 2021 to 65% in Q1 2022, according to Brightfield Group Consumer Insights data. With the average retail price of an ounce at $100 since October 2022, 75% of Michigan consumers now shop at recreational dispensaries in Q3 2023. Meanwhile, from Q3 2021 to Q3 2023, purchasing “through a friend or dealer” in Michigan dropped from 50% to 37%.

Adult-use shoppers in Michigan skew female at (56%), and a large percentage of purchasers are Gen Xers or Baby Boomers (40%). 69% of Michigan consumers report they use flower and 67% use pre-rolls—a close margin for the two product types. Michigan’s adult-use consumers are more likely to purchase gummies than the average recreational shopper in other states but aren’t as likely to pick up other product types. Even with prices so low, 80% of Michigan recreational shoppers say price is their top-ranked product attribute—more than taste, desired effect, or dosage.

For brands and retailers, Michigan is a battle to be won. No two dispensary menus are the same, with each competing for its piece of the $6.4 billion dollars spent on recreational cannabis since December 2019, according to CRA data through Oct. 2023. Stores offer their own brands—such as Lume Cannabis Co., one of the state’s top 3 retailers for purchasing—which has a full suite of products. Cultivators, infusers, and extractors vary by geography, but even dispensaries within the same town have unique items afforded to them by the array of brands available to stock.

While local brands abound, so do transplants. Per Brightfield’s H2 2023 study of Product Brand Health in Michigan, STIIIZY and Platinum Vapes have top awareness among vape users, while Cookies has the most loyal flower customers of any flower brand in Michigan. Multistate operators like PharmaCann, Ascend, and Cresco also are active with their suites of products, intensifying competition further.

Brightfield’s 2023 general population study of consumer wellness found 23% of Michigan cannabis consumers purchased cannabis in the past 3 months—6 percentage points higher than the national average (while alcohol and tobacco use are average). More operators mean more places to buy cannabis at an affordable price, more consumer normalization, and more dollars in the industry and for governments. While it might not mean the most profits for individual entities, it gives more businesses the opportunity to execute competitive innovations that ultimately delight consumers and move the industry forward.

Madeline Scanlon is cannabis insights manager for Brightfield Group.